As your editor I tend to get up very early – 5am in wintertime, 6am in summertime. As with all journalists I need coffee to turn in copy. Armed with my trusty Ikea cafetiere and strong Rwanda beans, being the shipping nerd I am I like my brew to be in a mug provided by the kind people at Yantian International Container Terminal (YICT). Every year at the TPM Asia conference in Shenzhen, YICT provides a mug (pictured) with its clients’ logos emblazoned around it. My cup from about six or seven years ago is now a bit of a collector’s item. At next year’s TPM Asia perhaps the marketing folk at Yantian might need to be handing out ristretto-sized cups given the contraction in liners seen this year.

Unquestionably, the shipping story of the year has been the five mergers in liner shipping and the collapse of Hanjin Shipping – all of which means that by 2018 there will be just 10 established global containerlines, down from 18 at the start of 2016.

In the festive period, families often tend to play board games. Growing up, a favourite after dinner for us was the game of Jenga, where each player has to delicately remove a wooden block and place it on top of other blocks without knocking over the whole tower. It was the fall of Hanjin at the end of August that dramatically quickened the pace of consolidation in the liner field. The South Korean’s collapse forced others to act fast – a logjam was washed away as lines sought partners to join the teu millionaire’s club.

From a journalistic point of view, the stories came in so thick and fast there was little time to react.

The merger, for instance, of the box subsidiaries of the Japanese trio of K Line, NYK and MOL, announced at the end of October, needs a little more coverage. Of all the mergers seen this year, on the face of it the coming together of an all-Japanese set of lines, all of whom had been set to join THE Alliance, a new container grouping in April, might appear the easiest assimilation of the lot. I would argue it is not. The job replications among the three are enormous as are the service offerings. My guess is this will be a very painful merger, but one we will not be privy to witness from the inside as Japanese corporate culture tends to make these sorts of things hard to fathom.

Sitting at the top of the container leaderboard is Maersk Line. Having moved to take over Hamburg Süd at the start of December, it commands an 18.7% global market share, with a combined fleet of nearly 4m slots.

Søren Skou became group CEO of AP Møller Mærsk earlier this year, and has since moved to split the group in two with an eye to selling its energy divisions and focusing just on transport and logistics. Skou was also the architect of the Hamburg Süd takeover. Listening to him speak earlier this month, Skou would have you believe that by 2022 there will be around 23m teu in global liner capacity against a likely demand for 22m teu.

Another container veteran, CC Tung, chairman of Hong Kong liner OOCL, reckons the liner supply/demand imbalance will remain imbalanced through till the end of this decade.

Both Tung and Skou are clearly presenting an underlying message to their peers – do not order more ships.

My feel, however, is that newbuild prices are now becoming just too cheap and, more importantly, political pressure in China to keep yards busy – and people employed – means we are going to see an inevitable raft of orders emanating from the People’s Republic in the new year. Nevertheless, the dramatic scrapping seen in the container sector this year – with some 700,000 slots taken out of service – is a hopeful sign that the worst is over for the industry.

Dry bulk turnaround

This time last year few would have predicted that as the final day of this very tough 2016 looms the sector with the best fundamentals is dry bulk. Dry bulk owners have been through the mill this decade but finally after much scrapping, the Baltic Dry hitting record lows in the first quarter and massive restraint when it comes to new orders, there is no segment in shipping with better investment potential than this one, I’d argue. And it’s not just me who thinks this. Just look at the big names who have been among the most active this year. Fredriksen, Blystad, Sohmen-Pao, Angelicoussis, Offer, Buttery – even Fred Cheng – these are all big, big names – and all of them have been on a buying binge, aware that the cycle is ticking over. Bear in mind too that as of late November the ratio of newbuilds to the extant dry bulk fleet slipped below 10% for the first time since 2002. The last time the orderbook ducked under this level heralded the start of the incredible dry bulk super cycle from 2003 to 2008. Now, despite the incredibly resilient Chinese bulk demand, I am not predicting a return to the $100,000 a day cape markets again, but I do feel this year’s canny investors are set to make very good returns on their ship acquisitions in the coming 24 months.

Tanker frustration

In the tanker segment, 2016 will go down as a year of frustration for owners. The year’s most marked trend has been its lack of any pattern and a growing sense of annoyance that rates did not work out quite as planned at the start of the year. For tanker owners, the fear is that the slew of tonnage coming out of yards in Asia in 2017 will mean decent earnings are now a way off. Tanker owners would do well to learn from their dry bulk peers – and indeed latterly their container cousins – they will need to scrap their way out of hardship in the coming 18 months.

Your thoughts

So that’s my very rough take on where the three main sectors are – by no means a vintage year for owners, though a great one for shipping journalists with so much happening. You too can have your say on 2017 prospects by taking part in our latest online survey called MarPoll. We’re asking readers whether next year will be any better for the various sectors in shipping. The survey needs no registration and has 10 simple questions posed. There is room for readers to leave comments by each answer if they want to expand on certain matters.

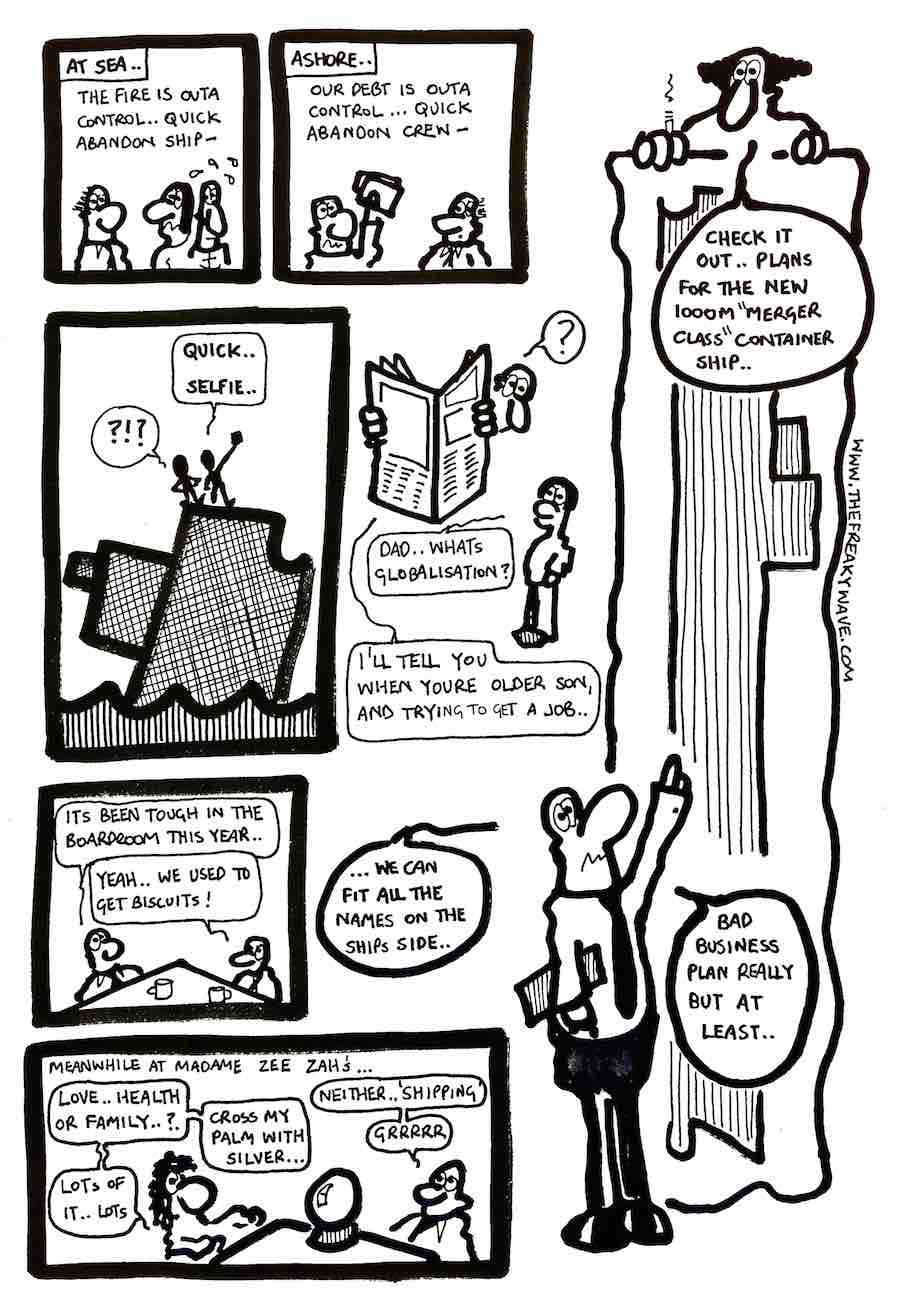

Finally, the year would not be complete without the thoughts of our resident cartoonist, The Freaky Wave, who deliberates below on what 2016 has meant for shipping.

Thank you for deciding to publish Dr Lynn Simpson’s exposés of her experiences of the live animal export trade. A fascinating, often upsetting, but never surprising look into the world on board live export ships. I discovered I knew a lot less about them than I thought I did.

I would like to second that comment. I was staggered that the shipping and logistics Press chose not to honour Dr Simpson with an award.

someone should make a documentary film out of this. why not?

After two years in the Offshore industry (after a career in tankers and dry bulk), I’m still unsure whether it’s actually Shipping. However, 2016 has been an awful year in the Oil and Gas sector, with thousands of seafarers and shore staff put “on the beach” as exploration activity plumbs new nadirs.

Posting this on New Years Eve 2016 with the only certainty that I will be working for a new Company and in a sector in 2017 – I just have no idea who or what.

Happy new year to all Splash; Editors, Contributors and Readers. Splash has covered the potential new movie (5 wedding and a funeral) extremely well. The only industry which has lost more players this year is the music and film industry. Enjoy the early morning beverages Sam – “no coffee, no workee”.

Keep up the good work in 2017.

I think you needed a category for “little change” which we should consider for some of the sub-sectors.