Does the ratification of the Ballast Water Management Convention spell gloom or boom for the dry bulk market? Will Fray from Maritime Strategies International investigates.

After more than 10 years in regulatory limbo, the IMO Ballast Water Management Convention will finally enter into force on September 8, 2017. Despite being beset with technical challenges and owners’ opposition, its implementation might provide the basis for a dry market recovery.

Following entry into force, all affected ships will be required to install a ballast water treatment system by the first renewal of their International Oil Pollution Prevention Certificate (IOPP), which is due at least every five years, during the vessel’s special survey. This effectively means that by 2022 all ships in the fleet must have a ballast water treatment system (BWT) installed.

Ballast water treatment plants and their installation involve a significant amount of CAPEX, with the level varying depending on the type and size, usually based on flow rate of the system and the technology selected, with cost ranging from $0.5 to $2m for a bulker. This is obviously a source of concern for the industry and individual owners alike.

Some vessels requiring a special survey in 2017 will be obliged to fit a BWT system, extending to all vessels with a special survey in 2018 and 2019. With the cost of a capesize third special survey in excess of $1m plus the additional outlay for retrofitting a BWT at around $1.5m, a 15-year-old vessel that is only earning $7,100 a day and worth $8.2m (based on MSI’s Q3 2016 forecast) the alternative of scrapping next year at $6.7m will look appealing to many.

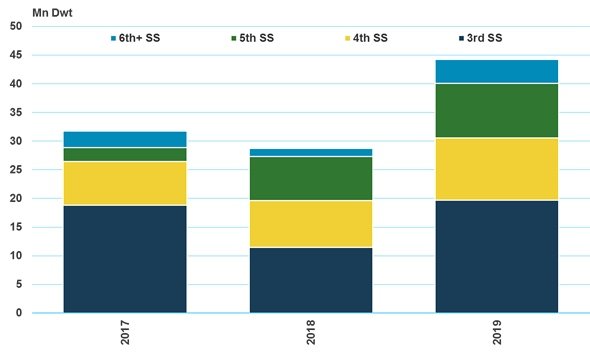

The chart above highlights exactly how many vessels in the dry bulk fleet will hit special surveys of three or more over the course of 2017 to 2019 based on age profile extrapolation. Of course some of these vessels will be scrapped before they reach these special survey dates but as an indicative position there is just over 100m dwt of dry bulk carriers currently on the water where the owner will soon have to make the call to invest or scrap.

In light of both the prolonged depressed state of the market and the imminent entry into force of the convention, we expect almost 100m dwt of bulkers to be removed over the course of the next four years to 2019. We expect deletions to be frontloaded, because owners will be almost immediately impacted by the parlous state of the market and have one eye on the entry into force timeline.

By the end of 2016 MSI expects 40.1m dwt of bulkers to have been removed from the dry bulk fleet, with scrapping falling to 26.6m dwt in 2017. Scrapping over the course of 2015 to 2017 will exceed all other historical triannual totals not only in dry bulk but also across any individual shipping sector.

This combination of low deliveries and high scrapping will be the driving force that will help pull the sector off the floor and provide a foundation for a recovery that will gain momentum at the start of the next decade.