The worst has already passed in terms of monthly fleet growth this year for dry bulk, writes Jeffrey Landsberg from Commodore Research.

January was a special month in the dry bulk market as it marked the worst in fleet growth having now come and gone (January often sees yearly surges in fleet growth). Prior to this year, this decade had seen an average of approximately 115 newbuildings delivered to the dry bulk fleet every January. This time around, though, January 2018 saw only approximately 60 newbuildings delivered. Taking scrapping also into account shows that the dry bulk fleet grew by a net addition of only about 50 vessels last month, which also marks the lowest January net addition seen this decade. Also of note is that prior to this year, this decade had witnessed an average net addition of approximately 80 vessels added to the dry bulk fleet every January. Going forward, much lower monthly newbuilding delivery totals and net additions will be seen during the rest of the year.

Overall, the net addition of 50 vessels added last month were absorbed into what has remained a healthy dry bulk market, and rates in several vessel classes ended January at levels similar to where 2017 left off. This was impressive considering how rates often fare in January. Panamax rates were even able to end up climbing in January due in part to the very robust global coal import demand seen that month. Going forward, the remaining months of 2018 are now likely to see net additions to the dry bulk fleet come in anywhere from five to 25 vessels per month (monthly dry bulk fleet growth will be lowest at the end of the year). There will certainly be significant volatility, however, but what is very encouraging is that nowhere near as high as 50 net additions are likely to be seen.

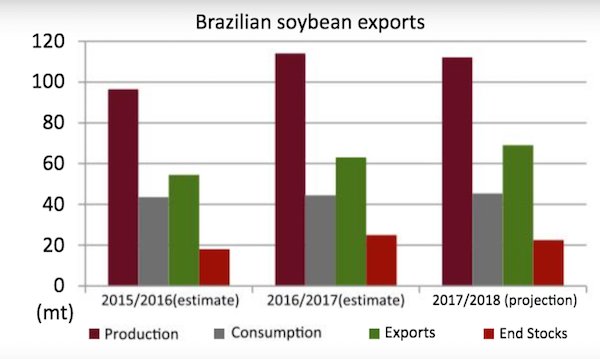

The worst in this year’s dry bulk fleet growth has already likely occurred, and that growth coincided with seasonally low overall cargo volume. What is new this year, though, is that the fleet growth was much lower than seen in previous January’s – and the trend of lower than normal fleet growth remains set to be seen throughout this year. At the same time, near-term coal, grain, and iron ore trade prospects also remain very encouraging. While the worst has come in this year’s dry bulk fleet growth, for the immediate future it is also simply terrific that the best has still yet to come in South American grain exports. Approximately 69m tons of Brazilian soybeans are expected to be exported during the current 2017/18 grain trade cycle, which would far exceed the robust 63m tons exported during the previous 2016/17 cycle and would also dwarf the 54.5m tons exported two years ago (See graph below). Most of the soybean cargoes will be shipped during the next six months, with the volume expected to be particularly strong during March through June.

Also significant is that, in total, Brazil and Argentina are expected to export around 64m tons of coarse grain during the current 2017/18 grain trade cycle. This would exceed the robust 62.5m tons shipped in 2016/17 and would dwarf the 39m tons shipped in 2015/16. South American coarse grain starts being shipped in earnest starting in June, and the vast majority of the cargoes are normally shipped in the second half of the year (with volume often peaking in September). Overall, near-term prospects for South American spot grain cargo volume are very encouraging. While the worst has come in monthly fleet growth, the best has still yet to come in South American soybean and coarse grain exports. Together, the dry bulk shipping market stands to benefit greatly.

This article first appeared in the just published latest issue of Maritime CEO magazine. Splash readers can access the full magazine for free by clicking here.