Capacity size gap between the largest carriers and the rest of the field now bigger than ever

The capacity size gap between the largest carriers and the rest of the field is now bigger than ever, according to data carried in the latest weekly report from Alphaliner.

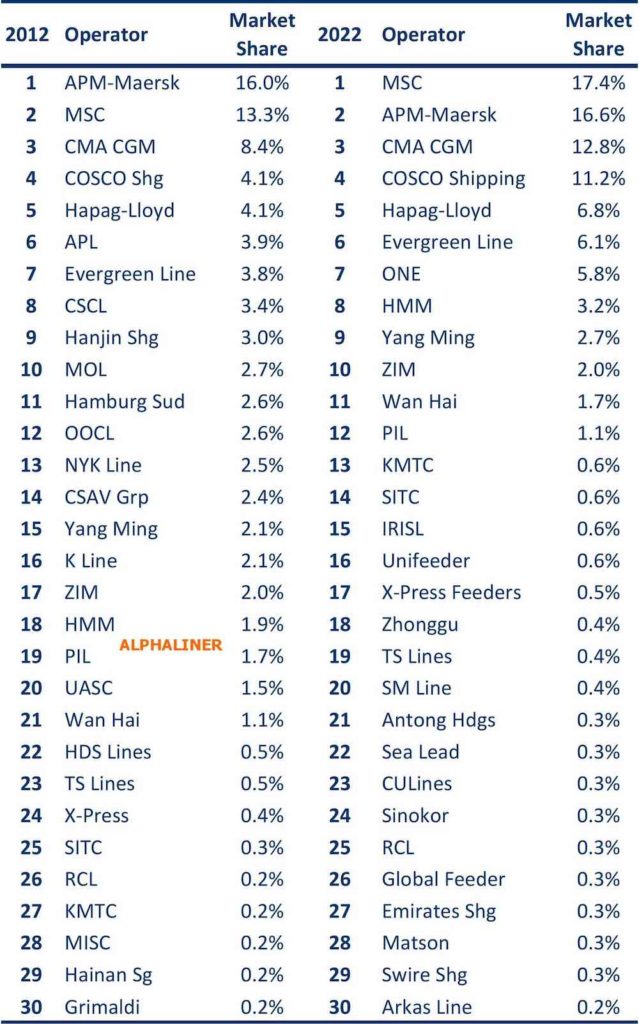

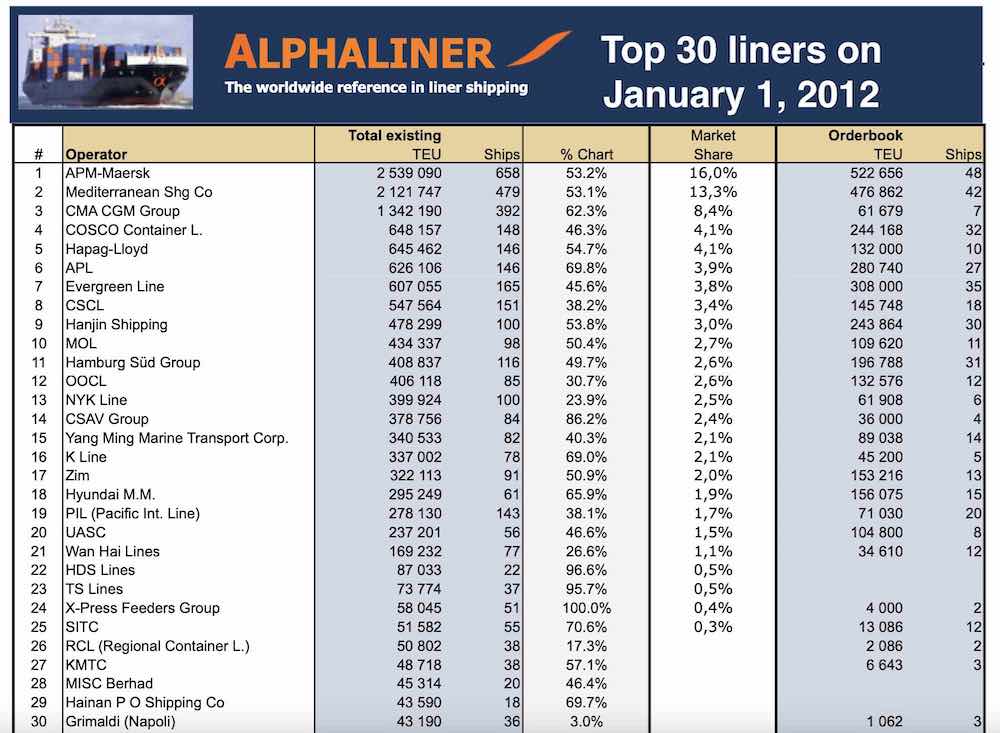

Today, the top 10 carriers operate 21.8m teu, versus 2.5m teu for the next 20 ranked lines, a far cry from the fragmented liner line-up a decade ago (see charts at bottom for 2012 rankings).

“Following widespread consolidation at the top of the table – consolidation that has attracted the attention of politicians and regulators – there is now a large gap between the leading carriers and the rest of the container field,” Alphaliner stated.

Larger lines have earned more proportionally too during the pandemic, Alphaliner data shows.

Earnings for medium and small lines typically increased by between 100% and 700% between 2019 and 2021. By contrast in the same period the top 10 carriers increased their profits by between 1,000% and nearly 6,000%, something that has raised the ire of shippers and politicians around the world with US president Joe Biden even going so far as to say earlier this summer that he’d like to have a “pop” at the global carriers.

Commenting on the potential for the gap between the top 10 and the rest to grow in the coming years, Splash columnist Kris Kosmala said: “I think the biggest carriers have the biggest cash reserves and they will spend their money on buying more ships, essentially squeezing the smaller players to the point that maybe they will hoist white flags.”

In well functioning markets, new firms – price fighters – will emerge to provide alternatives

Discussing the Alphaliner statistics with Splash, Olaf Merk, shipping expert at the OECD-affiliated think tank International Transport Forum (ITF), warned that such dominance has led to serious monopoly concerns.

Merk, a high profile campaigner against what he sees as liner shipping’s shift towards an oligopolistic market led by three consortia, said: “In well functioning markets, new firms – price fighters – will emerge to provide alternatives to the high prices of the established firms. In container shipping this does not seem to be happening. The consolidation of the biggest firms continues – as the data from Alphaliner shows – and the capacity of firms that are newly entering the container market is less than 0.5% of the total capacity – as our own data shows.”

It is not just the size of the global carriers themselves that has sparked concern with regulators and shippers alike during container shipping’s epic earnings run through the pandemic. The nature of the global alliances has also faced scrutiny. The three main global liner alliances account for more than 90% of all boxes shifted on the main east-west tradelanes.

Parash Jain, HSBC’s global head of shipping and ports research, discussed liner shipping’s stronger bargaining position thanks to consolidation last week in conversation with Splash.

“Going forward, we argue that after years of consolidation and the formation of mega shipping alliances, the shipping lines have learnt the capacity discipline and while there might still be volatility in freight rates, the rock-bottom level of freight rates seen in the past decade might no longer persist in the future,” Jain said.

Investigations by the US, the EU and others have repeatedly dismissed cartel claims over the past two years of extreme profit making for global container lines, but shippers continue to fight their case – most recently a gourmet food producer from Illinois suing Asian carriers Yang Ming and HMM over collusion claims.