Container carriers are embarking on a rates war, according to one leading analyst, while other experts contacted by Splash remain circumspect to label today’s diminished container earnings landscape as an all-out battle to the bottom.

Hua Joo Tan, who heads up research outfit Linerlytica, described the rates war as being “plain as daylight”.

“Carriers have given up all the April gains. Blank sailings are being removed, sailing speeds are rising, carriers have chased up charter rates,” Tan told Splash, going on to highlight some of the “funky” deals being offered by number two carrier, Maersk, adding that it was not just the Danish giant driving the rates battle.

“It takes more than a few names to drive a price war,” Tan stressed.

Alan Murphy, the CEO of container consultancy Sea-Intelligence, said that today’s market was “ripe” for a rate war.

“With already significant amounts of overcapacity, even more capacity coming on stream this and next year, and a weak demand environment, the market is ripe for a rate war, especially as carriers have overflowing war chests from the last couple of years,” Murphy told Splash.

Murphy said that it could even be argued that the unprecedented speed of the spot rate reversal constituted a rate war, especially as the carriers seem to have “overshot” the natural bottom of the market.

The Sea-Intelligence boss said there were three ways liner shipping could avoid a rate war. First, a sudden and completely unpredicted boom in container demand, of a magnitude close to the pandemic demand boom. Second, mass scrapping and lay-ups, and finally carriers learning to not accept loss-making cargo. Murphy does not see any of these three situations materialising, quipping: “The only thing that scares me more than shipping lines without money, is shipping lines with money.”

The only thing that scares me more than shipping lines without money, is shipping lines with money

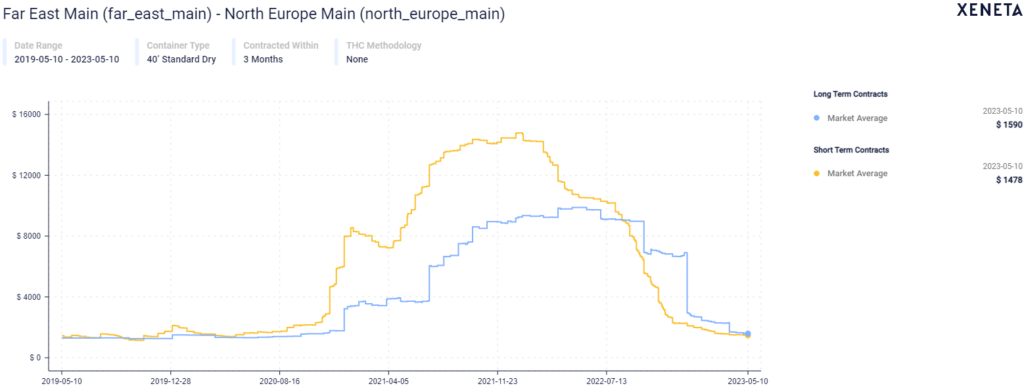

Peter Sand, chief analyst at Xeneta, a freight rate platform, argued that the rate war is already long gone, having been fought between the carriers last year.

“What we see have in May 2023 is a loss-making spot market for all of them,” Sand said, maintaining that the market continues to weaken by the day.

Jan Tiedemann , a shipping analyst at Alphaliner, said that after carriers had shown some restraint during Q1, a slew of big new ships are now being delivered, which will put pressure on rates.

Simon Heaney, senior manager of container research at Drewry, dismissed the talk of a rates war.

“This is a rate normalisation, not a rate war, if you look at the three-year roller-coaster of container freight rates,” Heaney told Splash.

After experiencing the highest and most profitable freight rates ever in most of the last two years, ocean carriers have conceded rates reductions in the last six months of 20-80% depending on the route on spot rates and rate reductions of 50-80% on year-long contract rates, Heaney explained.

“Carriers have not shown capacity discipline in the last six months, but rates remain at or close to pre-pandemic levels, which were fairly normal levels,” the Drewry analyst posited.

Also sceptical of the rate war talk was Lars Jensen, the CEO of container consultancy Vespucci Maritime.

“That is not what it looks like right now,” Jensen said, adding: “Seen from an overall perspective it appears we have reached a market bottom – worse in some trades than others, and the market is in a holding position waiting to see if we get a seasonal upturn in demand coming into peak.”

It has been clear since the middle of last year that the lines would be at each others’ throats in the middle or later part of 2023 (as I have advised many of my clients throughout 2022) simply because of the enormous order books of new tonnage about to be delivered and that same ordering spree is still continuing. Ad to that the already higher prices of charter prices being paid and one has to wonder if some of the liner shipping bosses are suffering from early onset dementia or are permanently hungover from their endless champagne parties.

True, the rates are back to the pre-pandemic level but we didn’t have the enormous slew of tonnage that is currently being delivered across many deep-sea trades and the combination with weaker and fluctuating Chinese output (not to mention near-shoring). The circumstances with 2019 do not apply to 2023 so the outcomes are likely to be different.

Based on the History (financial) of most carriers , they should be extinct. Someone is not being honest.

Shipping line made ton of money last 2 years .Charges customers 7x the price before covid