Further proof of how energy crunches drive freight rates is shown today in the suddenly booming LNG sector.

Splash has already highlighted how capes have traded higher in recent weeks in tandem with extreme demand and price hikes seen in the coal sector. The same is true for LNG, where major economies such as China, India and the UK are scrambling to fill holes in their national grids.

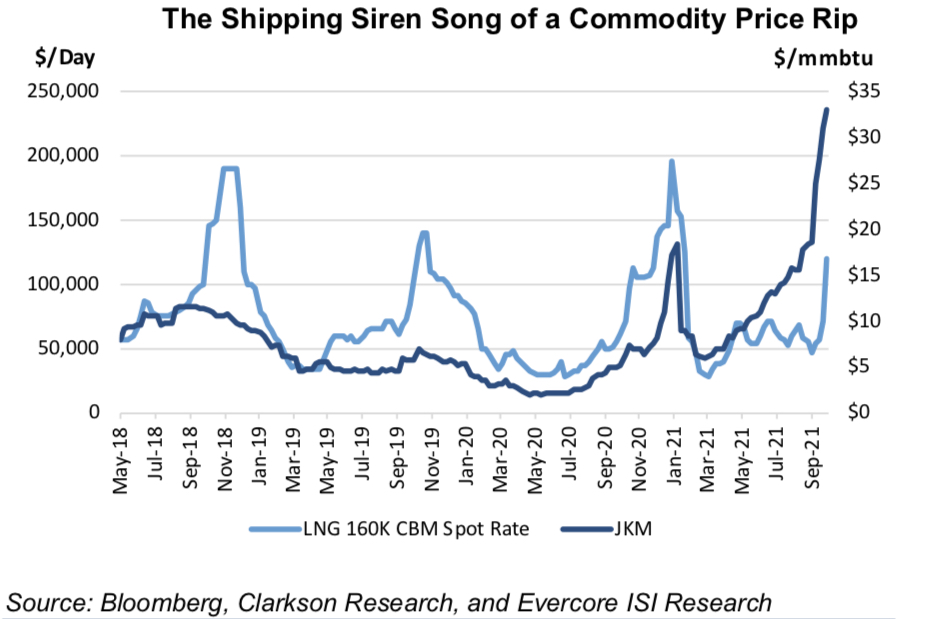

LNG shipping rates have followed the parabolic path of LNG prices in Asia and Europe, which have spiked to record levels in the past 10 days.

A new report from Evercore ISI shows LNG shipping rates for modern ships, which were languishing around $50,000 a day in late September, have more than doubled in the last two weeks alone with Fearnleys quoting $120,000 a day for 160,000 cu m TFDE vessels and Poten quoting $100,000 to $110,000 a day depending on the basin.

When demand-driven spikes drive commodity prices skyward, the ships needed usually join along for the ride

Evercore ISI has produced a chart (see below) highlighting the relationship between JKM (Asia) LNG prices and LNG shipping spot rates.

“[A]lthough the magnitude varies, directionally changes are often very similar,” the report from Evercore ISI states.

The JKM price for LNG has risen to an all-time high, with Platts assessing the November price at $56.326 per mmBtu on Wednesday last week. While it has since moderated back into the high $30s, it is still at historically high levels and a far cry from the year-low figure of $5.8 per mmBtu registered in February.

Data from Cleaves Securities show LNG freight rates saw another hike last week, with MEGIs adding 21% week-on-week to $109,000 a day, TFDEs +20% week-on-week to $85,000 a day and steam turbines up 32% to $69,000 a day.

Clarksons cited the wide open arbitrage out of the US and limited tonnage availability both East and West of Suez for last week’s spike.

On the correlation between energy prices and freight rates, Evercore ISI analysts added: “We could have easily chosen coal prices and Capesize spot rates from the dry bulk segment to show a very similar relationship, and as the energy shortage potentially deepens as temperatures plunge, there is a very good chance that the substitution of more abundant oil for coal and LNG could have a similar impact on the dour tanker market that is just starting to show signs of life.”

Concluding, Evercore analysts stated that the moral of the story is: “When demand-driven spikes drive commodity prices skyward, the ships that are needed to meet these needs usually join along for the ride. We’ve seen it in dry bulk and it is now being confirmed in LNG…are tankers next?”