New Year but same old shipping markets? Splash Extra examines the numbers.

During the Asian tiger economy years of the 1990s, the most the Baltic Dry Index (BDI) went up was by 34% in 1995, followed by a 34% correction in 1996 as the Asian financial crisis took hold. In 2006 the BDI averaged 3,180 then more than doubled to 7,070 in 2007 before it peaked and collapsed in 2008, ending up down 10%. Last year the BDI rose nearly threefold from an average of 1,066 in 2020 to an average of 4,948 in 2021. Capesize average earnings (based on the 5TC measure published by the Baltic Exchange) grew from an average of $13,000 in 2020 to $33,100 in 2021. Panamaxes (basis the Baltic’s P4TC average) went from $8,600 in 2020 to $25,400 in 2021, supramaxes from $8,200 to $26,700 and lowly handysizes tripled from $8,000 in 2020 to $25,700 in 2021.

But then in October China introduced its steel production cap and its three red lines policy of preventing over-leveraged property developers from borrowing more money. The BDI fell 61% from a peak of 5,647 on October 6 to end the year at 2,217. In January it has continued to fall, averaging just 1,923 points to January 21. The benchmark Capesize 5TC fell from $86,953 on October 6 to $19,490 at year’s end. In January it has continued to slide, reaching $7,390 on January 21, depressingly close to operating cost levels, though some brokers report that owners are refusing to fix at below $10,000 per day.

There is no smoking gun, no single cause that everyone can agree on for the fall in the market

Brokers and operators are blaming the weak market on lockdowns in China, the debottlenecking of ports in China, the Indonesian coal export ban, the easing of the Indonesian export ban, the Winter Olympics, Christmas and the western New Year holidays, a sudden surfeit of ballasters, rains in Brazil, a lack of rain in Brazil and Argentina, and even fog in the Bosporous (the fog of war in the Black Sea may come soon enough). In other words, sentiment is almost universally negative but there is no smoking gun, no single cause that everyone can agree on for the fall in the market. Where is the Sue Gray figure whom the market can agree has caused the lockdown party to end? (Sue Gray is the UK civil servant tasked with establishing whether rule-breaking parties happened in Number 10 Downing Street while the general population was not permitted to meet family or friends).

The fundamentals of supply and demand remain in owners’ favour. 431 bulk carriers delivered in 2021, totalling 39.41m dwt, of which 13.43m dwt was capesize and 5.84m dwt was VLOC tonnage. In the last year, 60 ships of 6.6m dwt were sold for demolition, giving net fleet growth of 32.81m dwt, or 4% – hardly enough to cause this market meltdown on the back of such strong demand growth in 2021.

Whatever the reason, key freight routes are plummeting. In the Pacific, the leading capesize round voyage route C5 is down to $6.7 or thereabouts even as iron ore prices have recovered to levels last seen in October last year at the peak of the freight market.

In the Atlantic, the C3 Brazil- China route is down to $17.60 from a peak of $47+ in October. It is back to levels last witnessed in March 2021. Rains in Brazil did cause a hiatus in loading cargo at key iron ore export ports. The rainy season tends to last for much of the first quarter of every year but has been heavier than usual this year.

Presumably the cargoes will be backlogged rather than lost, if port productivity can be optimised later in the year. As this seasonal effect is annual, Vale appears to be sanguine and has not downgraded its export estimates for the year of the usual 320-350m tonne range.

In the grains markets, hot and dry weather has damaged South American soya and corn crops. The US Department of Agriculture suggests Brazilian soy and corn production is down 8m tonnes from their previous forecasts for this crop year. The Rosario Grain exchange suggests even lower yields. But this is for Q2 – why would it affect markets now?

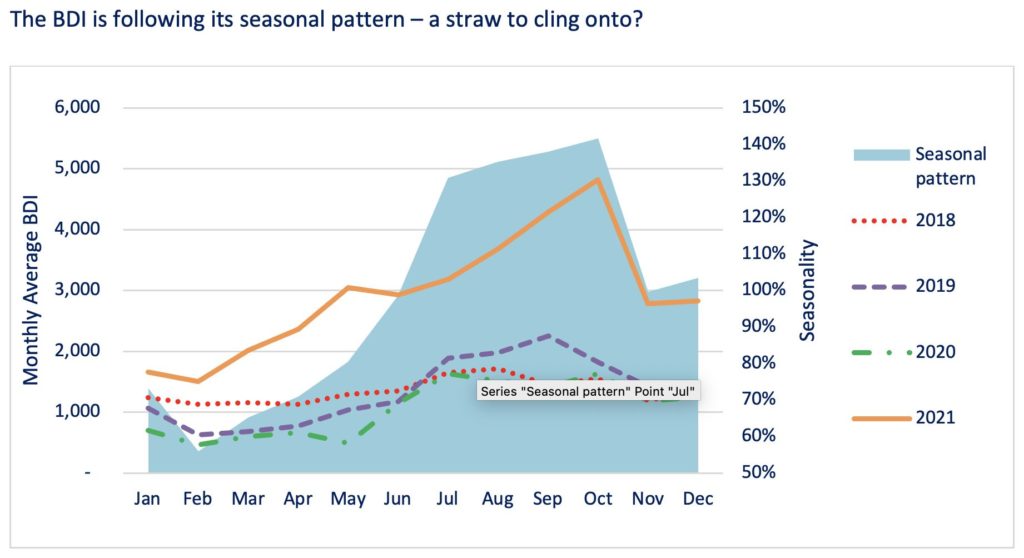

Is this it for the current market cycle which began at the start of 2020? There is hope for operators. Earnings were last at these levels a year ago around Lunar New Year 2021. The BDI has followed exactly the seasonal pattern of the last several years by peaking in October and bottoming out around Lunar New Year, before going on a nine-month bull run. If the BDI can average more than 1,658 points this January, it will be ahead of January 2021 already. So perhaps this year won’t get going until we have all said gong hei fa cai.

This is an extract from the regular markets commentary published in Splash Extra, a monthly subscription title. Published on the last Wednesday of every month and priced for as little as $200 a year, Splash Extra serves as a concise monthly snapshot, ensuring readers are on top of where the shipping markets are headed. For more details on Splash Extra subscriptions, click here.