Sharply contrasting fortunes from two Korean conglomerates last week have sparked conjecture on whether newbuild prices will head further north.

Hyundai Heavy Industries, the nation’s largest shipbuilder, reported a Q2 loss last week, citing soaring steel plate losses for its red ink performance, while Posco, South Korea’s top steel mill, registered an all-time record quarterly result.

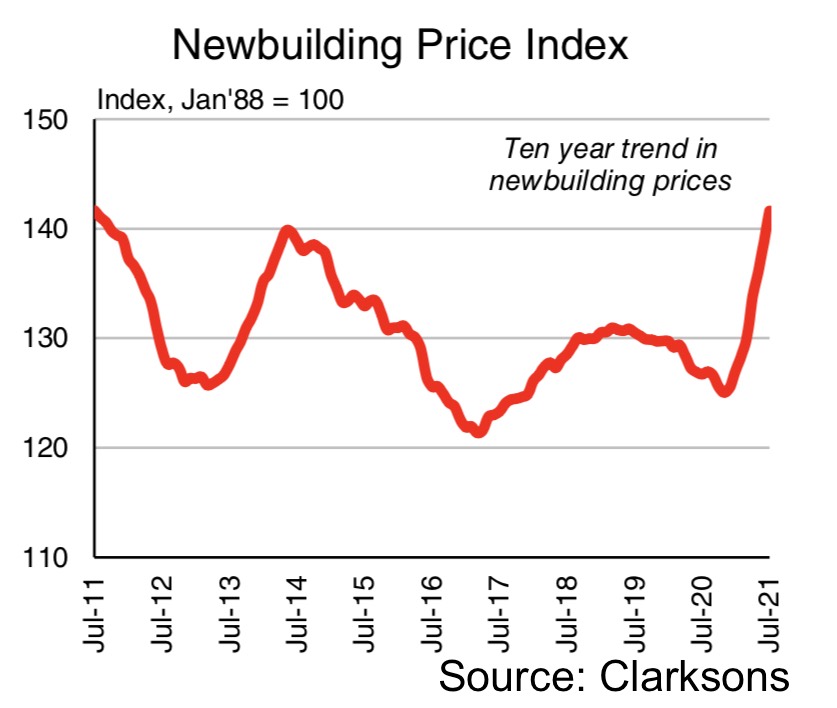

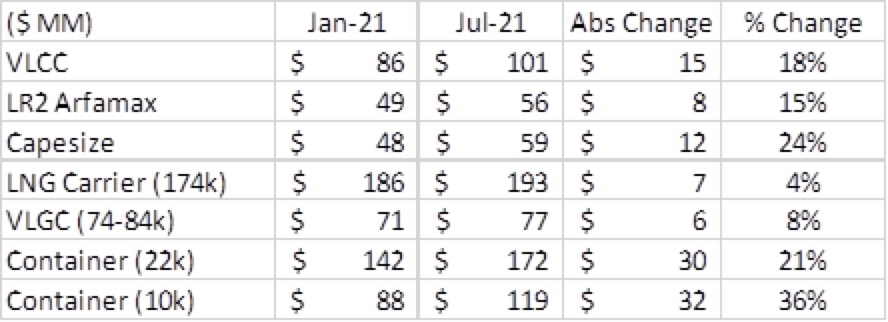

According to Cleaves Securities, newbuild prices have risen by 12% year-to-date, the majority of the price increase down to higher steel prices. A VLCC newbuilding has increased by $12m in steel costs alone this year.

Yards aren’t necessarily in a better position as the slots fill up

“Against our overall view of increasing newbuild ordering over the next years due to a prolonged period of underinvestment in shipping, we expect newbuild prices to rise further,” commented Joakim Hannisdahl, Cleaves’s head of research.

Rebecca Galanopoulos Jones, head of research at brokers Alibra Shipping, pointed out that yards have already this year put some contracts on hold until there was more clarity over steel prices and then, in many cases prices were renegotiated higher.

“Any future price rises will very much be driven by sentiment in the direction of steel prices,” Galanopoulos Jones said.

Add in a weak dollar with negative real interest rates and prices look like they can only go upward

Mark Williams, who heads up British consultancy Shipping Strategy, argued that the shipbuilding sector is still in “defensive merger mode” and is yet to be convinced about growing capacity.

“Price pressures should continue to increase especially with new tech to meet emissions goals and the general increase in commodity prices. Add in a weak dollar with negative real interest rates and prices look like they can only go upward,” Williams suggested.

“Given no let-up in steel prices, full near-term backlogs and the favourable container outlook, I wouldn’t be surprised to see prices creeping up,” said Jonathan Chappell, a shipping analyst with Evercore ISI, adding that for the first time in many years shipyards were in greater control at the negotiating table thanks to their suddenly swelling orderbook.

Running contrary to this theory, Dr Roar Adland, shipping chair professor at Norwegian School of Economics, told Splash that the growing orderbook ought not to be seen as a sign of bargaining strength for the shipyards.

“It is risky for the shipyards to lock in contracts for vessels that they won’t even start building until two years from now,” Adland pointed out, reminding readers of the time post-financial crisis when owners, having paid a 10% deposit, had no qualms about walking away from their contracts when the markets went sour. Also, shipbuilders have a hard time locking in their input prices that far ahead, which makes their ultimate profit highly uncertain.

“All told, yards aren’t necessarily in a better position as the slots fill up,” Adland maintained.

Randy Giveans, senior vice president of equity research at Jefferies, cautioned readers on yards’ actual capability of pushing through further sizeable prices increases, noting the continued hesitancy of many owners to order newbuildings due to both the uncertain demand outlook and the unclear environmental/emissions regulations as well as the significant spread between newbuilding and five-year asset values.