In the first of two-part special Dr Martin Stopford from Clarkson Research provides a condensed maritime history, arguing that the future of the industry is very much in smart shipping.

Commercial shipping changes slowly, with only three major “waves of change” since Vasco Da Gama sailed to India in 1497-8, opening global ocean navigation and trade. The most recent, “bulk shipping”, started in the 1950s. Since then the commercial shipping business model has relied on economies of scale to reduce unit freight costs. Under this system ships are stand-alone production units, run by small companies with tight overheads. But the business model is facing diminishing returns; shortage of skilled officers and endless quality and regulatory supervision. This paper argues that changes in Information and Communications Technology (ICT) make a new business model viable. The “Smart-Shipping” model focuses on the transport performance of the company/fleet as a whole, rather than a collection of individual ships, resulting in wide reaching improvements in transport productivity; safety; personnel development; and logistics.

Proposition 1: The maritime business model can change

What happens if the shipping industry is confronted by a radical new technology? For example technology which allows a fleet of ships to be run significantly more efficiently and safely? Such changes do not happen often in shipping and there have been three only major system changes in the last 500 years, each very traumatic. In the 16th Century it was global navigation; in the 19th Century it was steamships serving empires and in the 20th Century it was global free trade and bulk shipping systems.

Wave 1 (1497-1815): global sea trade – lateen sail, rudder, compass

The first was ocean navigation. Although shipping has a 5,000 year history, it was only 500 years ago that seafarers got comfortable with global navigation. Before then maritime trade was local, operating within six areas – NW Europe, the Baltic, the Mediterranean, the Middle East Gulf, the South China Sea, and the North Indian Ocean.

Navigators kept close to the coast and navigation between regions was limited, though not unknown (e.g. the Vikings discovered N America, China sailed into the Atlantic etc.). These early explorers discovered, but then went home with no interest in building new trade routes. The European navigators in the 15th century were very different. They were searching for new trade routes to the Spice Islands, to replace the overland routes which had become less accessible. After a century of Atlantic exploration, mainly by Portugal, in 1497 Vasco Da Gama made the first voyage to India, mapping the route and bringing back a (small) trade cargo and the more important knowledge of the massive price arbitrage in the pepper trade. They used the latest technology, but some of it had been around for centuries. This included the lateen sail, a centerline rudder and navigation instruments including the compass and the astrolabe, which allowed them to make landfall with reasonable precision during long ocean voyages.

This first wave of innovation lasted three hundred years from about 1490 to 1790. During that period the business was mainly about treasure, trade and land. The big achievement was to map the world, establishing trade routes, mainly in the Atlantic and trading centers, for example the plantations in the Caribbean and E Coast N America. Shipowning hardly existed as a profession and much of the navigation was highly speculative and relatively unstructured, due to three technical problems. Firstly ships built with wooden hulls and masts were small, only 200-300 tons; secondly reliance on sail and wind made voyages slow, unreliable and very risky; thirdly there were no communications between regions, so trade was difficult to organize. Innovation was patchy and during the 18th century, between 1741 and 1814, the cost of freight increased.

Wave 2 (1815-1950): Imperial trade – steam engines & steel hulls

The next wave lasted from 1815 to 1950. All three problems were solved. Fossil fuels powered steel hulled ships which could be built to almost any size and sail to a schedule. Communication by cable was gradually improved (cable, telephone, telex etc). The driving force was the need for a sea transport system to link Europe to North America and Asia and to serve the European Empires, which it made possible. The shipping industry developed into the liner and tramp system which was a complete solution (but commercial sailing ships were still trading in the 1930s).

Institutional issues were crucial. This was an imperial era and the new shipping system carried passengers, cargo and mail between colonial states and their colonies. Small ships were needed to access colonial ports and conference systems stabilized rates; tramp vessels were designed to switch between charters to the liner companies and trading in bulk on the spot market; and much bigger passenger liners which operated on some routes, especially the North Atlantic, carrying passengers and some cargo. It was an enormously productive period.

The business was managed by large national shipping lines carrying mail, passengers and general cargo. Many were ‘household names’ and they were supported by tramp shipowners operating small multideck vessels which could charter to liners during the busy season, otherwise carrying bulk or “tramping” general cargo.

The liner and tramp system lasted for 100 years during which time the fuel consumption of ships measured in Kg/000 ton miles was reduced by 85% from 88.9 kg/000 ton miles to 12.2 Kg/000 ton miles. But the small, labour intensive, liners and tramps became increasingly uneconomic as cargo volume and handling costs escalated after 1950.

Wave 3: Free trade – diesel engines & welded steel hulls

In the 1950s the European empires were disbanded and the world economy was opened up for trade. Cheap long haul freight for multinationals importing raw materials and exporting manufactures was the new driving force. Small, versatile steamships powered by coal were replaced by much bigger and more specialized welded ships with diesel engines burning oil, operating out of purpose built terminals. Improved navigation, radar and better communications all contributed to reducing costs. This industrial shipping was orchestrated by the multinational companies – oil companies, steel mills, grain traders and feed compounders. They sponsored the construction of very big ships, designed to carry bulk cargoes such as oil, ore, coal, chemicals, gas, cars, and forest products at very low cost. So far this wave has lasted 65 years and resulted in the construction of a deepsea cargo fleet of 58,429 standard and specialized ships covering every size of vessel required to carry every size of cargo moved by the global transport system. Fuel efficiency has been reduced by a further 79% from 12.2 Kg/000 ton miles in 1935 to 2.6 Kg/000 ton miles today for an 18,000 teu containership at 23 knots.

Real freight costs fell between 1950 and 1970, but then in the 1980s began to rise again. Meanwhile the business model for shipping bulk cargo had changed. Initially the multinationals shipping cargo built up the their own fleets of tankers and bulk carriers or chartered newbuildings on long time-charter from independent shipowners (in liner trades the liner companies went down a similar route, had to set up the system themselves and they did not get started until the 1960s and outsourced to the KGs). But as the bulk system matured in the 1970s, the shippers drew back, leaving independent shipowners to manage investment within the framework of the market, trading on the spot market. This resulted in a business model in which ships were flagged out; services were subcontracted and company staff was often restricted to only 1-2 people onshore for each ship at sea. This system offered a plentiful supply of ships at very low cost. In many ways it represented a return to the neoclassical economic model of the 19th century in which small companies drove prices down to marginal cost.

Although this business model produced cheap freight, in recent years the slim management structure has presented cargo interests and regulators with growing concerns over quality, safety and pollution. The result has been a growing focus on monitoring and inspection of ships by regulatory authorities, port states and charterers.

Another problem with this neo-classical business model is that horizons for innovation are inevitably short.

Typically one year payback is fine; two years needs board approval; and beyond three years gets deferred.

Resolving these issues are difficult because different participants – shipowners; cargo owners; shipyards; design companies; engineering companies and the classification societies – have little common ground, with no natural leader of change. The charterers, the natural leaders, have become less involved in the management of the transport business than previously, their transport managers tended to focus exclusively on getting a cheapest transport available today, not to develop strategy. Since the shipowners take their lead from their customers, this is a significant issue in managing change.

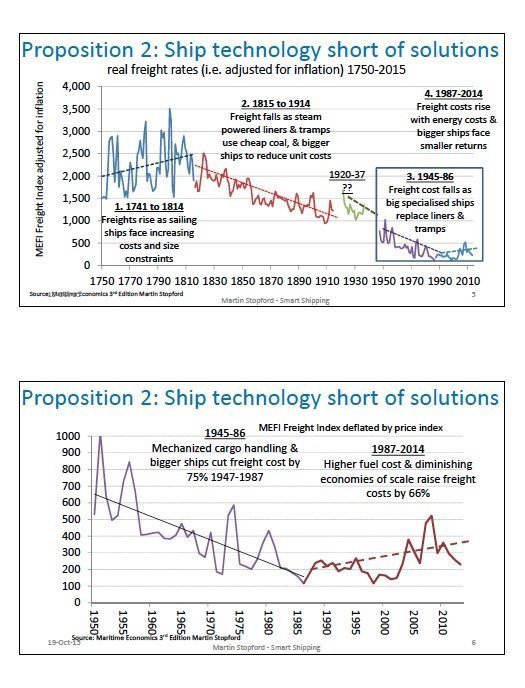

Proposition 2: Marine technology is running out of solutions

The business model is unique in the modern industrial world, characterized by many small companies relying on highly speculative market earnings. In 2014 there were 39,000 deep sea ships run by 7,729 companies, an average of 5 ships each. Small tramp companies are not new, but compared with previous generations of tramp owners, today’s business model combines a debt heavy balance sheet with slim overheads and little secure revenue cover and an arm’s length relationship with their customers. To make these companies bankable, ships are generally treated as stand-alone assets for mortgage purposes, with a liquid market for employment and asset trading. Typically the shipping company holds the shares in the one ship companies registered under an open flag, with a small staff on shore. Budgets are kept tight by cyclical markets, returns are low and investment horizons are short. This is a cost minimization business.

The problem faced by investors is that after fifty years of building progressively bigger ships and fine tuning their design and engineering, the industry is running out of ways to cut costs. Since the 1980s the real costs of freight has been on a rising trend, because after 150 years the ship design technology has been squeezed so hard that there is not much left to squeeze. On the engineering front, diesel engines are close to their theoretical energy conversion ceiling and for 30 years there has been little efficiency improvement. For example the fuel consumption of 60,000 dwt bulk carriers delivered has been around 32 to 33 tonnes per day since the late 1980s. Recent ecoships claim about 28 tonnes per day, but this is mainly due to fine tuning in response to high fuel prices rather than any fundamental improvements in efficiency. Naval architects are still designing ever bigger ships, but the economies of scale diminish with each size increment.

However the pressures for improvement continue relentlessly. One is from the high cost of fossil fuels; another from the regulation of emissions from engines burning fossil fuels; thirdly the IMO commitment to cut the carbon footprint generated by moving 10+bn tonnes of cargo a year by 50%; and finally people – the crew and customers want a better deal. But as the technology wave the industry started surfing 150 years ago loses momentum, each step along this this well-trodden path of improving the hardware gets smaller.

Click here for part two and how the industry can embrace smart shipping.