Clarksons Research has drilled down to show subscribers to its weekly newsletter the severely skewed global orderbook, and the ramifications for this unbalanced contracting in the years ahead.

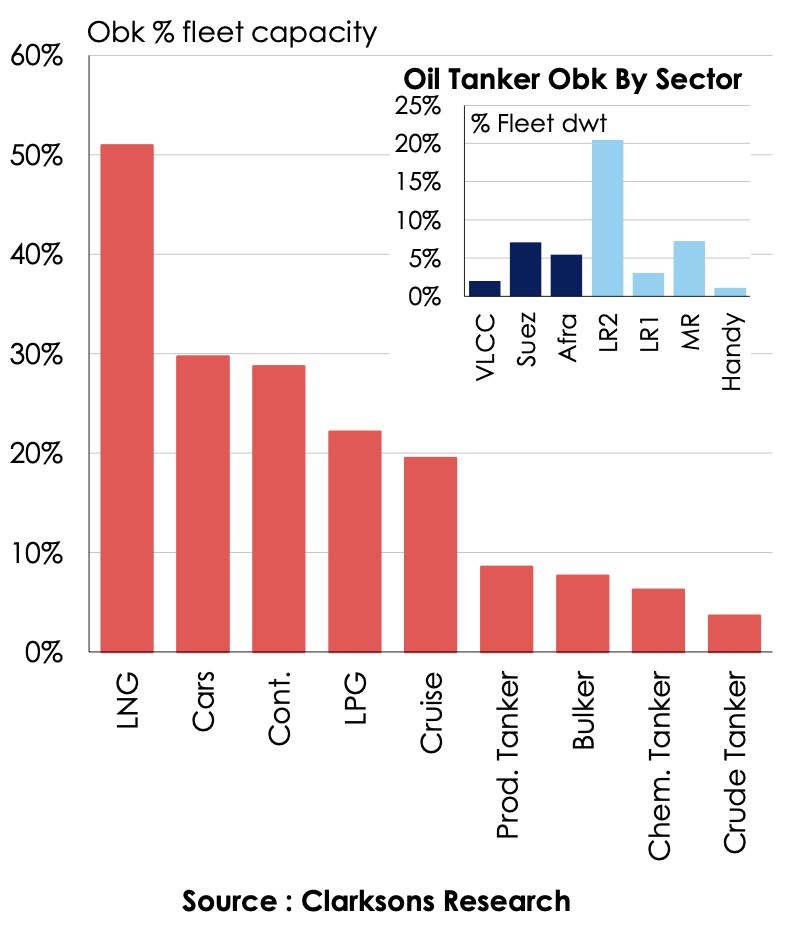

Clarksons data (see chart below) clearly shows how highly divergent the orderbook is across sectors, with the British outfit describing the current situation as a “two-speed” pattern.

LNG carriers top the chart, with a record orderbook of 55.7m cu m, double the start 2022 figure and equal to over 50% of the fleet, while bulker and tanker orders are well below the historical average.

The huge variations have a range of implications, Clarksons explained. Even if overall shipping fleet growth remains moderate – with Clarksons projecting 3% per annum growth across 2023-24 – parts of the fleet will experience much stronger expansion than others. LNG fleet growth is projected by Clarksons at around 10% in 2024, whilst across 2023-24 boxship fleet growth of an average 7% per annum is projected, versus around 1% per year in tankers.

For investors and builders, there will be impacts from variation in lead times for new orders, Clarksons pointed out. The average time to scheduled delivery for LNG carrier contracts placed this year stands at 48 months, versus 31 for containerships, 29 for product tankers and 27 for bulkers.

While tanker newbuild contracts have picked up significantly in the first seven months of this year, the orderbook remains close to all-time lows.

Data from Jefferies shows tanker ordering has increased though the size of the orderbook has risen marginally from 4% at the start of the year to 5% currently.

Analysts at Xclusiv Shipbrokers, meanwhile, maintain that the global tanker fleet is in danger of shrinking in the near future mainly because of the low orderbook, which stood at its lowest point since 1996 in February this year and because about 34% of the active fleet is older than 16 years.

For dry bulk, Cleaves Asset Management argued in a recent report that the limited supply side will set the stage for a significant recovery in the sector, starting in the second half of 2024.

“The orderbook to fleet ratio remains low at 7%, and we expect net fleet growth of approximately 2.5% per annum from 2023 to 2025,” Cleaves stated.