Some observers – including 65% of Splash readers in our latest ongoing poll – believe shipping demand and GDP have decoupled, threatening container shipping demand. Not so fast, says James Frew, senior analyst at Maritime Strategies International.

After the swingeing downwards revisions made to trade forecasts in our Q3 2016 container market outlook, our Q4 report has only seen marginal adjustments. Unfortunately however, marginal adjustments are far and away insufficient to dig the industry out of the colossal hole finds itself in.

Trade growth is living down to our expectations, and rather than 2016 being the year where the industry saw some sort of recovery it is now feared that, instead, it marks a new normal where growth in containerised trade is slower than overall economic growth.

It is certainly the case that container trade volumes over the past five years have been depressing, and 2016 sees this trend worsening. Growth in global container trade in 2015 was just 1.7%, and 2016 will see that slow even further to 1.6%. However, whereas in 2015 the principal culprit was negative Asia-Europe trade growth, in 2016 the slowdown has been more broad.

Asia-Europe westbound volumes in 2016 are expected to remain basically flat (up by 0.4% yoy), whilst Transpacific eastbound cargoes are estimated to have grown by 2.3%. The non-mainlane trades are little better, with the intra-Asian trade at 2.2% and cargoes on most southbound Latin American and African trades sliding into negative territory.

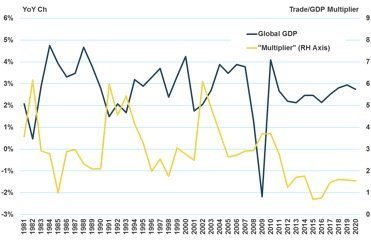

Chart 1: The trade/GDP ‘multiplier’ has not been at a steady level for the last 20 years, and the relationship between global GDP growth and container trade is less stable than commonly assumed. We are currently seeing the lowest levels of the multiplier since the 2000s, but this is not without precedent as data from the 1980s & 1990s show similar levels. The current slump is not necessarily a ‘new normal’.

Even so, MSI believes this ‘decoupling theory’ to be somewhat overblown. Firstly, the industry has always implied that the relationship between GDP and container trade growth is far closer than it actually has been. Chart 1 above rams this home, plotting global GDP growth and the multiplier to container trade.

As the chart shows, the GDP multiplier has never been at a steady level, and analysts looking at a multiplier in the period 1983-1991 would have come to a very different conclusion to those looking at it from 1991 to 2004.

Chart 2: Even the three most stable regional GDP multipliers have fluctuated over recent decades. Again, we see that the 2000s were more of an outlier. This is why MSI are sceptical of claims that the current state of the industry represents a ‘new normal’, even if demand growth remains lacklustre as we move into 2017.

In general, the GDP multiplier is an extremely blunt tool, and this becomes apparent when we examine it on a regional level. Chart 2 above shows the more stable of the regional GDP multipliers. Latin America’s trade/GDP multiplier oscillates between 8 and -11 on an entirely unpredictable basis (and also occasionally heads off into the plus/minus four figure range), whilst Europe is nearly as volatile.

North America’s trade GDP multiplier has been more stable, but also shows the fallacy of talking about historical multiples as if they are immutable. Instead, the multiplier for North America was – stripping out the -11.5 data point seen in 1991 – relatively stable at around 1.5 for the 1980s and 1990s.

The 2000s saw the container trade multiplier boom to over three times GDP growth, driven by the trend of outsourcing manufacturing, principally to Asia. The last five years have meanwhile seen a multiplier of around 1.4 for North America.

In other words, for an outside observer with no knowledge of the industry, a reasonable assumption might be to strip out the 2000s and suggest that the period we are currently in very much resembles the 1980s and 1990s.

We are not so sure that this naïve assertion is as far off the mark as many industry observers would suggest. Of course, overall the 1990s saw strong cargo growth, in part boosted by ongoing containerisation of breakbulk but also boosted by a global economy in a strong recovery phase.

The last five years have indeed seen very slow trade growth, but also economic growth at a pretty anaemic level, with the global economic growth figures being severely juiced by Chinese growth at over 6%. All of the above is simply to suggest that MSI is deeply sceptical of the current industry discussion about a ‘new normal’ of terminal decline in container shipping demand.

It is certainly true that trade growth this year has been exceptionally disappointing, but given that we now know that economic growth has been weak and factoring in the additional uncertainty stemming from Brexit and the US election, we are not sure it was justifiable to expect much better. Instead, we think that talking about a ‘new normal’ is only really relevant if we disregard the evidence of the 1980s and 1990s and just take container trade data from the 2000s and compare it to the present.

Is there any good news? 2017 is expected to see container trade growth recover to around 3.7% and 2018/19 are expected to see the rebound strengthen to around 4.5%. However, it is worth emphasizing that this 4.5% growth represents a cyclical highpoint, boosted by the weak growth levels seen over the past two years: 2020 will see growth slip again.

Has the historic link between global GDP growth and shipping volumes actually decoupled? Have your say now by taking our latest online survey, MarPoll – it takes two minutes to fill in and there is no registration. To take the survey, click here.