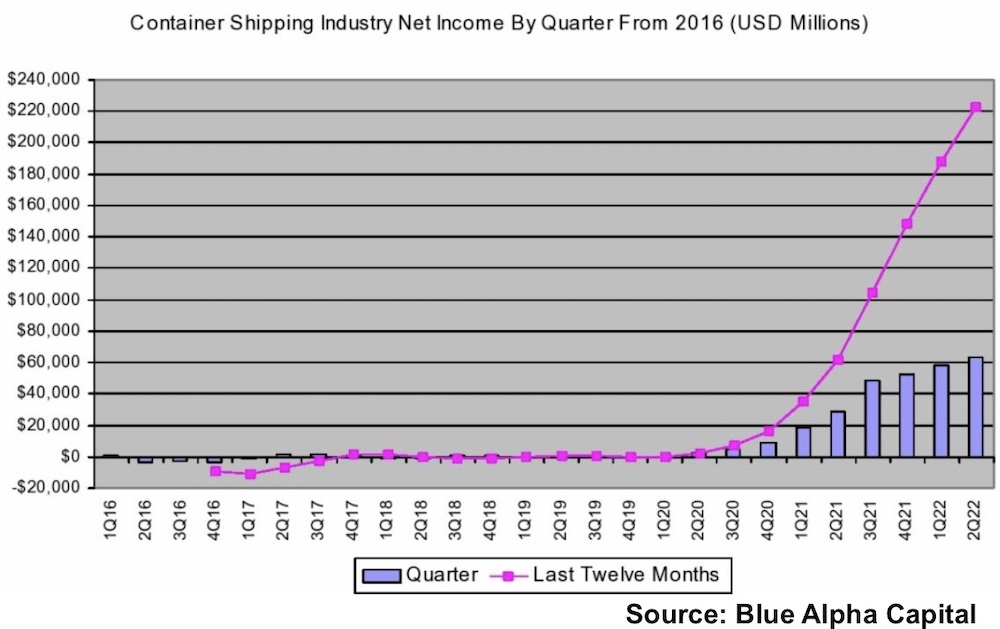

Q2 results for global liner shipping have surpassed what has ever been reported by any company in the historically low margin transportation sector, according to a new report from container veteran John McCown, who heads up Blue Alpha Capital.

Seven individual container shipping companies had Q2 net income higher than UPS, consistently the most profitable transportation company in the world, with these carriers actually more than twice as high on average compared to the American logistics giant.

The combined net income of UPS, Fedex, Union Pacific and JB Hunt in Q2 was $5.5bn, just 8.6% of the earnings of the container shipping industry. Collectively, the net income to revenue margin of those leading US transport companies was 9.2% in the second quarter of 2022, just one-fifth of the actual container shipping margin.

Comparing liners to the FANG quartet – namely tech giants Facebook, Amazon, Netflix and Google – also highlights the rarified atmosphere container shipping has entered over the past year.

The folks who focus on spot rates and are predicting a near term earnings collapse are substituting narrative for analysis

Container shipping industry profits were 14% higher than total FANG profits in Q4 last year, 103% higher than FANG profits in Q1, and 145% higher in Q2. Moreover, the container shipping industry’s net income to revenue margin of 46.1% in Q2 was four times the overall FANG margin and still almost twice as much if low margin Amazon is excluded.

McCown has tallied the results of 11 global liner operators that issue financial reports, who represent nearly two-thirds of total capacity, while assuming the remaining non-reporting operators had similar per teu results to develop the overall container industry results.

McCown argued that too much focus had been spent by analysts and media this year on the declining spot market, which he said accounted for only 10% of boxes shipped. Contract rates remain massively elevated and are the reason McCown is forecasting liner shipping will make a cumulative net profit of $244.9bn for the full year of 2022, a remarkable 65.2% improvement over 2021’s record results.

We may be at or near the peak, but no earnings collapse is imminent

“The folks who focus on spot rates and are predicting a near-term earnings collapse are substituting narrative for analysis and will be proven wrong. We may be at or near the peak, but no earnings collapse is imminent,” McCown wrote.

A key tool to watch, according to McCown, are blanked sailings. “Look for that to be a key driver of the industry’s performance for the balance of 2022 and in the years beyond,” McCown predicted.

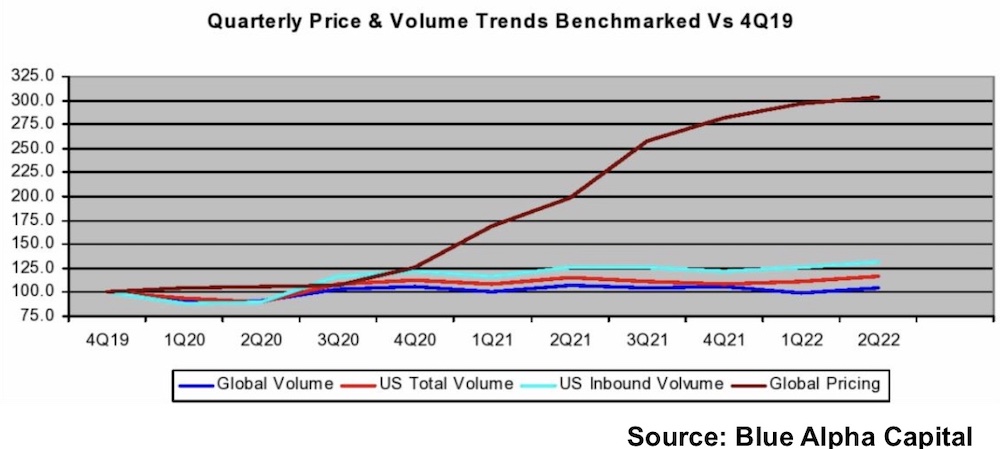

Data from Container Trades Statistics (CTS) shows that worldwide container volumes were down 1.6% in the second quarter compared to the same quarter last year, extending a downtrend from the 1.2% volume decline in the first quarter.

Many other analysts are voicing caution about liner prospects. The demand-led spikes seen during the pandemic that propelled container shipping to record earnings are now a thing of the past, according to recent analysis from Copenhagen-based Sea-Intelligence.

Sea-Intelligence has run the numbers on supply and demand during the covid era, and its conclusions add to the growing consensus that volumes are slipping, and it is only supply chain chaos such as port congestion that is helping prop up rates.

Global demand was consistently at a level 10% higher than capacity, from November 2020 to January 2022, according to Sea-Intelligence.

However, the gap has been narrowing, and the most recent data from June, shows a gap down to 2% versus the pre-pandemic levels.

“All in all, what the data shows is that the extreme spikes in freight rates in 2021 were indeed driven by a situation where demand suddenly exceeded capacity at a global level – but it can also be clearly seen that this was an effect primarily driven by the unavailability of capacity,” Sea-Intelligence argued.

The recent trend towards normalisation has in turn also been primarily driven by gradual improvements in schedule reliability and vessel delays, Sea-Intelligence suggested, going on to predict that the supply/demand balance will continue to decline, and freight rates will be under increasing downwards pressure.

Sea-Intelligence warned yesterday that trends on the transpacific ought to worry carriers.

Long-term rates are beginning to follow the trend set by the spot market

“As of now, scheduled capacity deployed on both Asia-North America trades for the upcoming weeks is considerably higher Y/Y, which will likely outpace even the most generous assumptions of demand growth. If this level of capacity deployment is maintained, utilisation levels are likely to drop even further, causing a downwards pressure on freight rates,” Sea-Intelligence stated in its most recent report.

The Shanghai Containerised Freight Index (SCFI) spot box freight rate index stood at 2,848 points on September 2, down 10% week-on-week and now down 44% on the peak at the start of 2022, albeit still more than three times the 2019 average. Rates on the Shanghai-US west coast route fell by more than 20% week-on-week to $3,959 per feu.

While long-term box freight rates continue to climb they are finally showing signs of coming under pressure.

Data from online platform Xeneta shows that long-term rates increased 4.1% in August, standing 121.2% higher than this time last year.

Nevertheless, there are signs that new long-term contracted rates are actually starting to drop on key trading corridors. However, due to the fact they’re replacing expiring agreements with considerably lower rates, the average paid by all shippers is still climbing.

“Volumes are dropping and, as expected, long-term rates are beginning to follow the trend set by the spot market,” Patrik Berglund, Xeneta’s CEO, commented last week.

Unveiling record quarterly results on Friday, Rodolphe Saadé, chairman and CEO of CMA CGM, became the latest high-profile liner executive to highlight the changing fortunes in the container trades.

“The global decline in consumer spending, which was already perceptible this summer, will lead to more normal international trade conditions in the second half as well as to a downturn in shipping demand,” Saadé said.

Not quite The South Sea Bubble but certain similarities.