Shipowners have every reason to be satisfied with the start of 2017 but a weaker Q2 could set the stage for further slowdowns, says Will Fray, senior analyst, MSI.

Dry bulk shipowners and operators could be forgiven for feeling very satisfied by the end of the first quarter of 2017. In its latest quarterly dry bulk market report, MSI notes that a quarter on quarter increase in rates above 5% in this period is relatively rare, having occurred on only three occasions since 2004. In 2017, capesize, panamax and handymax vessels fared far better, increasing 25%, 26% and 23% respectively.

Strong demand played a key role in better freight earnings this year and MSI’s forecast for global iron ore imports has been increased by 30m tonnes in 2017 and coal by 40m tonnes, partly driven by recent robust trade data and positive global steel output.

Rates have deteriorated from their March/April highs however. By early June, capesize spot rates had fallen to below $9,000 a day, supramax to $8,000 a day and panamax and handysize both close to $6,000 a day.

In its previous report, MSI attributed better capesize rates early in the year to strong iron ore demand in China which continued into Q2. According to Reuters’ vessel movement data, Australian exports in the first five months of the year were up 3.3% year on year, while those of Brazil were up 5.2% year on year. The combined exports of the two totalled 490m tonnes over that time period, up 16.3m tonnes year on year.

Spring surge is sprung

Since then, iron ore volumes into China have slipped, with MSI’s assessment of deadweight demand from the these capesize routes falling from a monthly average of 159m dwt in the first quarter, to 149m dwt in April and May.

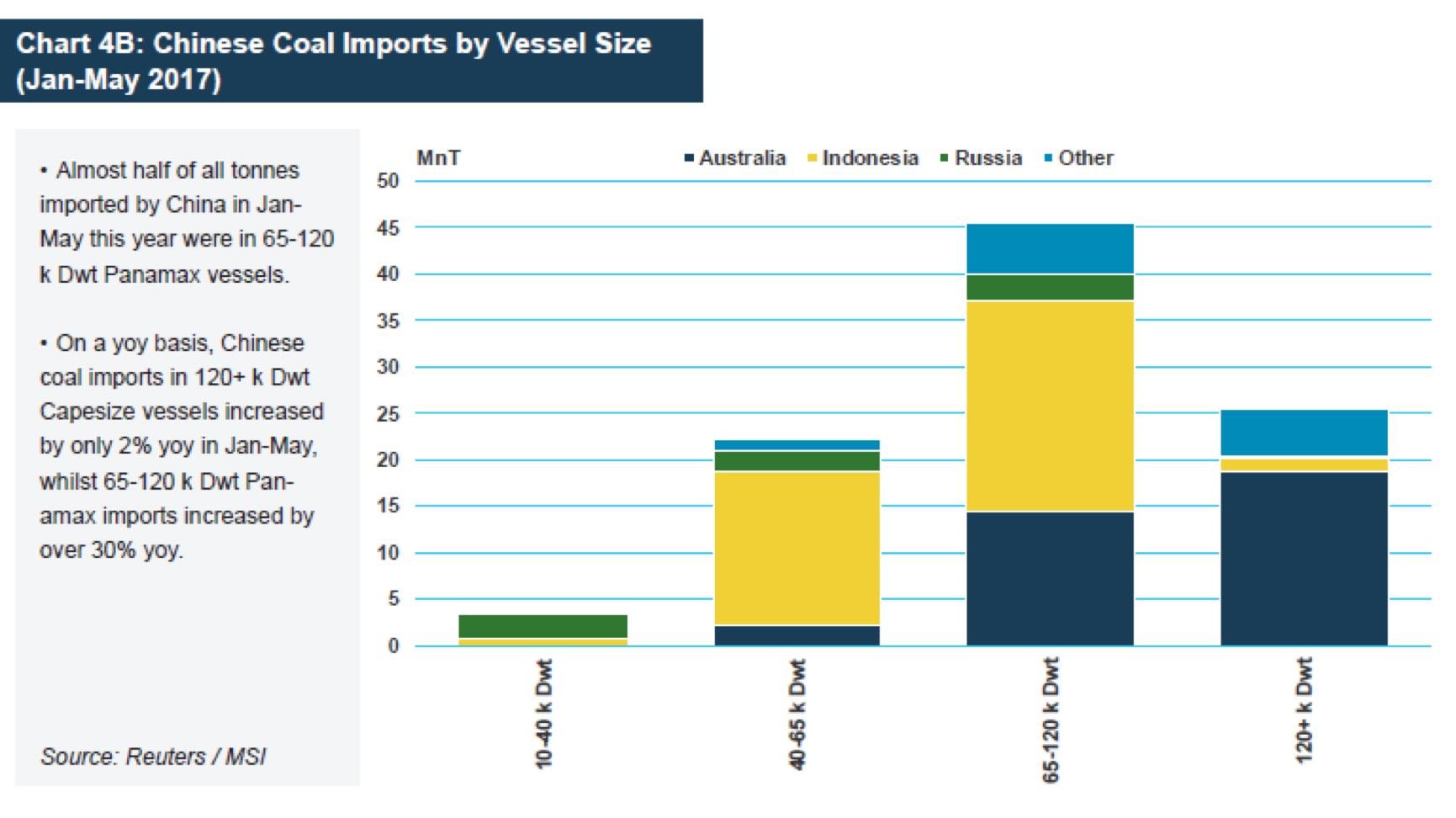

Coal shipments have increased to China this year (by 17% year on year in January-May), although this has less impact on the cape market, as a larger proportion of coal is transported in sub-capes.

Chart 1 (4B) shows that almost half of all tonnes imported by China between January and May this year were in 65-120,000 dwt panamax vessels. Of this, half were in standard 65-75,000 dwt panamax types, 14% in kamsarmaxes and 18% in 90-95,000 dwt post-panamaxes.

Moreover, on a year on year basis, Chinese coal imports in 120,000+ dwt capesize vessels increased by only 2% between January and May, whilst 65-120,000 dwt panamax imports increased by over 30% year on year.

On a forward-looking basis, MSI expects dry bulk sector rates to weaken further in Q3 on the back of a slowdown in Chinese demand for iron ore and coal, and lower expectations for US grains shipments as we enter the 2017/18 crop year.

MSI is cautiously optimistic for Q4, expecting resurgent iron ore trade to push average capesize one year time charter rates higher, to over $14,000 a day on average. Beyond this timeframe, MSI expects the market to continue to improve in 2018 thanks to aggregate commodity trade growth of 2.7% year on year (or 124m tonnes) and fleet expansion of just 0.4% year on year, increasing average sector employment rate to 85.1%, pushing time charter rates up 5% year on year on average.

Downside risks increasing

This relatively rosy outlook masks some significant downside risks to MSI’s outlook in the near term, of which the most significant is a potential slowdown of China’s dry bulk imports.

Indeed, some macroeconomic lead indicators now signal a downturn in industrial activity, with clear ramifications for raw material imports. Last month, Moody’s downgraded China’s credit rating from A1 to Aa3 to reflect how China’s financial strength will erode due to continuing high levels of debt, and China has recently tightened certain policies related to access to credit.

Indicating tighter credit, M2 money supply growth dropped below 10% year on year in May for only the third time since 2000. Tighter credit and an increase in short term interest rates has also been blamed by some analysts for a 30% year on year fall in refined copper imports for the year to date; copper is considered a bellwether of the Chinese economy given its importance in the construction and energy sectors.

The June 28 announcement that China plans to ban coal imports starting July 1 at some smaller ports hit values in the FFA market. Preliminary analysis suggests the impact of the ban will be minor, although this development serves to reinforce the risk related to fluid government policy in China.

Additionally, there is a possibility that China will step up its commitments to close down industrial capacity with much greater vigour in Q4, to ensure compliance with 2017 calendar year targets.

This is certainly a downside risk for steel output, given MSI’s Base Case forecast for production growth this year to be a four-year high of 2.4% year on year. The potential impact on MSI’s forecast for domestic iron ore mining has less downside risk – MSI’s base case forecast of a 27% year on year fall in both 2017 and 2018 would in any case be all-time records and compare with a 16% year on year average fall over the past three years.

China modelling

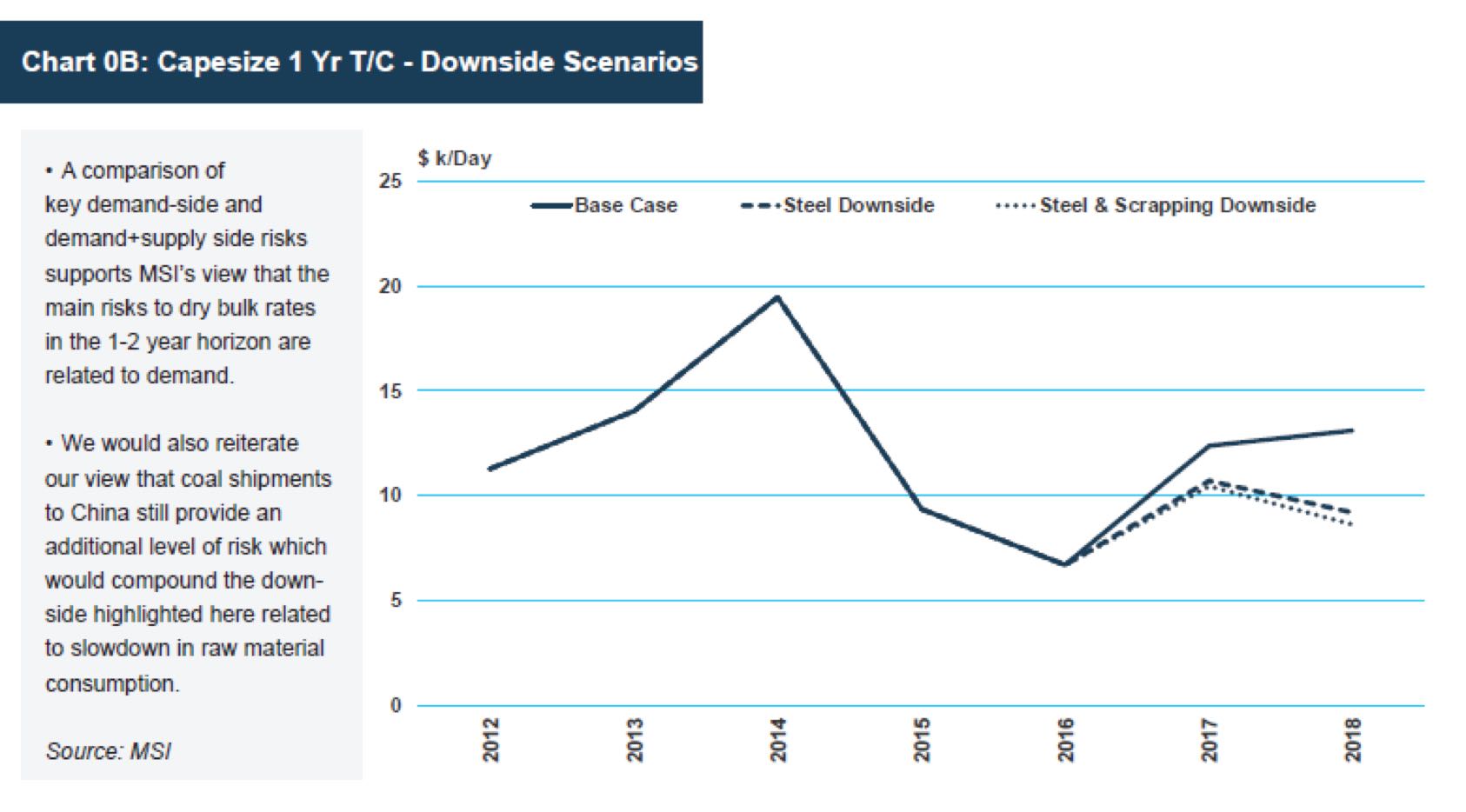

In an attempt to place this downside risk into context, MSI has formulated a scenario by which Chinese steel output falls by 2% for the remainder this year and next. Without changing any other driver in its model, our capesize one-year time charter forecast would be almost 50% weaker than the MSI base case for 2018, and would fall year on year, as illustrated in Chart 2 (0B).

If, in a low case, we assume China’s steel output falls by 2% year on year for each remaining month this year and next year as a whole, and we do not change our iron ore production forecast, then we would expect iron ore imports of 1,080m tonnes this year, and 1,098m tonnes next – the latter down 70m tonnes (6%) from the MSI base case.

This change alone brings about a 15m dwt reduction to the MSI demand forecast which would result in a downturn in the dry bulk fleet employment rate next year – rather than 85% employment in the base case, this would drop to 83%. Capesize one year time charter rates would be 20% below the base case, falling year on year instead of rising.

The chart compares the impact of two scenarios on capesize one year time charter rates; one the impact of lower Chinese steel production alone, and the other the impact of both lower Chinese steel production and also lower scrapping combined.

This comparison supports MSI’s view that the main risks to dry bulk rates in the one to two year horizon are related to demand rather than supply. However, it also reiterates the view that coal shipments to China still provide an additional level of risk which would compound the downside risk related to slowdown in raw material consumption.