The European sanctions have now taken full effect on Russian coal as of Thursday, something analysts are confident will have a positive effect on the global dry bulk tonne-mile picture.

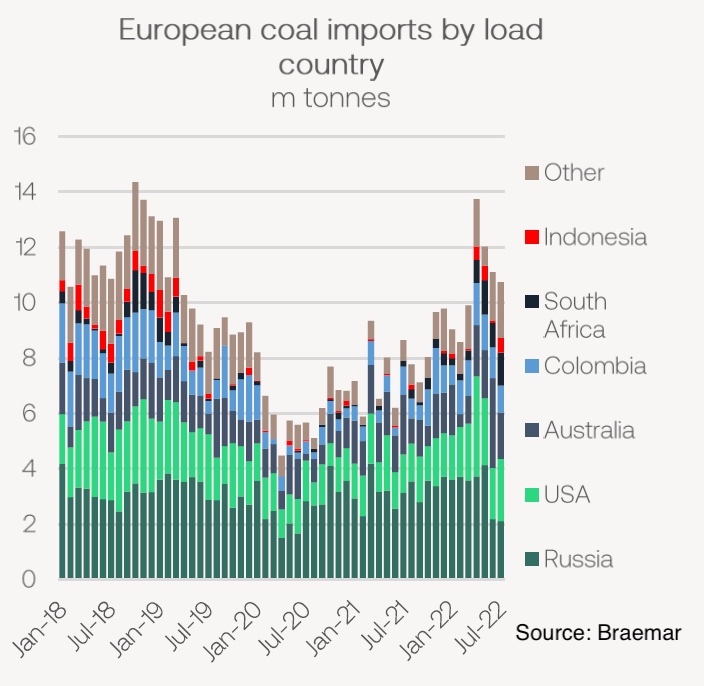

In 2021, the EU imported 39m tonnes of coal from Russia, totalling some 36% of the bloc’s coal imports.

The EU’s demand for coal has increased year-to-date and is expected to increase further as the bloc turns to coal to replace missing natural gas supplies from Russia.

The most basic upshot of the total ban will see more Atlantic and Australian coal heading into Europe and most Russian coal moving east to India and China.

Historically, Europe has had little to no effect on the demand intensity of seaborne coal trade, analysts at Braemar noted in a new report.

“Since the war started, however, we can see the positive effect European coal imports have had on bulk carrier demand. This is not only a reflection of the longer voyages, but also simply the greater volumes imported,” Braemar pointed out.

Not only is bulk carrier demand from coal improving due to European imports from further afield, it is also down to the change in flows out of Russia. Russian coal imports to India doubled year-on-year in July to 1.9m tonnes, according to Braemar data, while China imported 6.8m tonnes, a 22.7% year-on-year increase and the highest monthly total on record for this trade.

Of concern to European utilities scouring the globe for urgent coal supplies was the decision this week by the Indonesian energy and mineral resources minister to ban 48 miners from exporting coal.

Niels Rasmussen, chief shipping analyst at BIMCO, commented: “The EU’s ban on Russian coal increases demand for non-Russian supply by about 4% and a sustained partial ban of Indonesian exports will obviously not help. It makes it even more likely that India and China will buy more of their coal from Russia in the coming months. Combined, the two shifts in supply patterns will drive up average sailing distance for global coal shipments and bulk demand overall.”

Logistically, the heatwaves that have dominated the European summer are creating bottlenecks with inventories at ports in northern Europe at highs not seen for many years as barges struggle to make it down the parched Rhine river.

Soaring natural gas prices are giving rise to coal demand around the world, with consumption set to match this year the record-high from 2013, and further jump to a new all-time high next year, the International Energy Agency (IEA) said at the end of last month.

Fitch analysts have substantially lifted their Asian thermal coal price forecast for this year and beyond.

Fitch now expects the fuel loaded at Australia’s Newcastle port to average $320 a ton this year and $246 a ton on average from 2022 to 2026, up from previous outlooks of $230 and $159, respectively.

So, instead of a green gas from bad but close Russia, Europe will use more dirty coal from good but remote Australia? How do all that comply with European green agenda?

The new gas line from Portugal will reduce the need for coal.

The main problem is that Germany abandoned nuclear and the FF industry and AGW deniers are still holding back wind and solar. You can blame the ERG/GWPF/Exxon, but some are too scared.